")

da-kuk

Artificial Intelligence (AI) could be the next technological revolution to follow cloud computing, and we’re just scratching the surface of its capabilities. While there are countless scenarios where AI will create advancements throughout society, there is no doubt that it will also be used in nefarious ways. Cybercrime has been on the rise, and whether you’re an individual or a major corporation, everyone is a potential target. In 2022 the Federal Bureau of Investigation (FBI) received more than 800,000 cybercrime related complaints with losses exceeding $10 billion. This is just what came into the FBI, as the estimated cost of cybercrime globally in 2022 was $7.08 trillion. As advancements in AI occur, cyberattacks will become more sophisticated, and the need for cybersecurity will continue to increase. In September 2023, Cisco Systems (CSCO) announced that they would acquire cybersecurity company Splunk (SPLK) in a $28 billion all-cash deal. The cybersecurity industry is expected to grow significantly in the coming years, and after looking into the top companies, I am getting very interested in Fortinet (NASDAQ:FTNT). FTNT is trading at an inexpensive valuation compared to its peers, the underlying financials are strong, and its growth should continue as the total addressable market (TAM) for its products expands. I feel that FTNT is a long-term opportunity and could potentially be acquired if consolidation continues in the cybersecurity industry.

Seeking Alpha

The cost of cybercrime continues to grow and Fortinet is at the heart of mitigating cyber risk

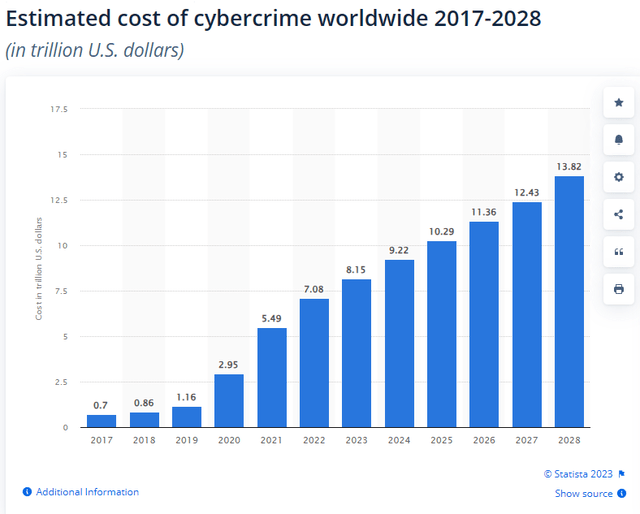

The ramifications of cybercrime continue to increase at a staggering rate. The estimated annualized cost of cybercrime worldwide from the close of 2017 through 2022 increased by roughly 911%. In 2017, there was roughly $700 billion of damages related to cybercrime, which will increase to $7.2 trillion in 2022. The global impacts of cybercrime are projected to increase from $7.08 trillion in 2022 to $13.82 trillion in 2028 as YoY growth is expected to continue. According to Forbes, cybercriminals can penetrate 93% of company networks, and in 2021 businesses suffered 50% more cyberattack attempts compared to 2020 on a weekly basis. Roughly 43% of all data breaches involve small and medium-sized businesses, while 83% of these businesses are not financially prepared to recover from a cyberattack. Roughly 20% of small companies do not utilize endpoint security, and 52% do not have in-house IT security experts.

Statista

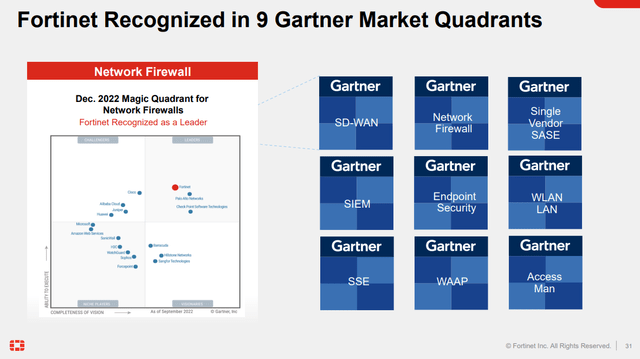

There are many cybersecurity companies that operate on the hardware and software side. Gartner has recognized FTNT in 9 market quadrants, including SD-WAN, network firewall, single vendor SASE, SIEM, endpoint security, WLAN LAN, SSE, WAAP, and access man. FTNT was recognized as a leader in network firewalls, SD-WAN, and Enterprise firewalls. More than 70 analyst reports, including Gartner, IDC, and Forrester rank FTNT as one of the most validated cybersecurity companies globally. FTNT is a global leader in cybersecurity and networking solutions for organizations, including enterprises, communication service providers, security service providers, government organizations, and small businesses. FTNT focuses its enterprise solutions on secure networking, cloud security, AI-driven security operations, FortiGuard Security Services, and support and professional services.

Fortinet

FTNT operates in both the product and service side of cybersecurity as they have their own line of networking products and cloud services. FTNT’s core products include their Core Platform firewall product family, which includes firewall, intrusion prevention, anti-malware, VPN, application control, web filtering, anti-spam, and WAN acceleration. On the service side, FTNT has its FortiGuard security subscription services which are designed to deliver threat detection and prevention capabilities to end-customers worldwide. In Q3 of 2023 FTNT generated $465.9 million of revenue from its products and $868.7 million from services. This was a 0.6% decline YoY in products but an increase of 21.63% increase YoY in services. For the first 9-months of 2023, FTNT has seen its product revenue grow 16.03% YoY to $1.44 billion and its Services revenue increase 29.38% to $2.45 billion.

Fortinet

I am getting interested in Fortinet because of its financials, growth, TAM, and valuation

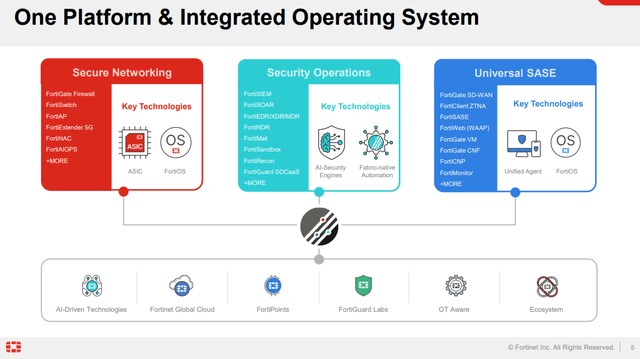

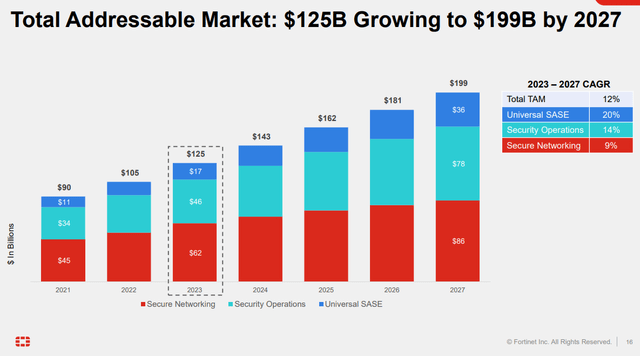

The total addressable market for FTNT currently sits at $125 billion, with secure networking representing $62 billion, security operations at $46 billion, and universal SASE at $17 billion. This is expected to grow to $199 billion over the next 3-years to $199 billion by 2027 as secure networking grows at a 9% CAGR, security operations grows at a 14% CAGR, and universal SASE grows at a 20% CAGR. There is a large opportunity for FTNT over the next several years, especially as cybercrime becomes more proficient through the utilization of AI. FTNT is at the forefront of utilizing AI-driven technologies to strengthen its product offerings through its security processers, FortiOS, and global cloud network.

Fortinet

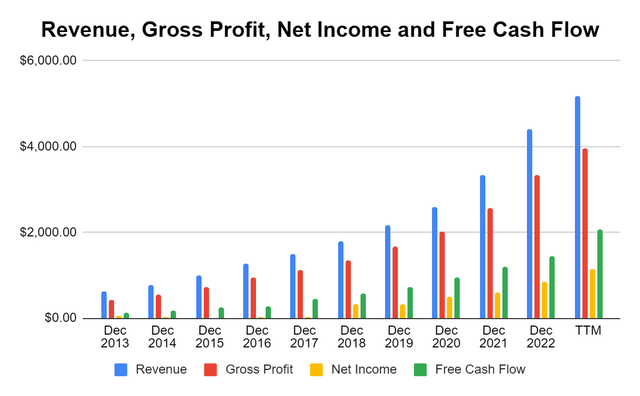

After going through FTNT’s financials, I am impressed. FTNT has been growing its top-line YoY and producing profitability on an annualized basis over the past decade before Free Cash Flow (FCF) became a buzzword in 2022. In the trailing twelve months (TTM), FTNT has increased its revenue by $755.3 million (17.1%) on a YoY basis. This has allowed its gross profit to expand 18.65% to $3.95 billion, its net income to increase 34.22% to $1.15 billion, and its FCF to grow 42.39% to $2.06 billion. FTNT is operating a highly profitable business as its gross profit margin is 76.44%, its profit margin is 22.25%, and its FCF yield is 38.9%. Over the past 3-years since the close of 2020, FTNT has grown its annualized revenue by $2.58 billion (99.38%), its gross profit by $1.93 billion (95.32%), its net income by $622 million (135.56%), and its FCF by $1.11 billion (115.47%).

Steven Fiorillo, Seeking Alpha

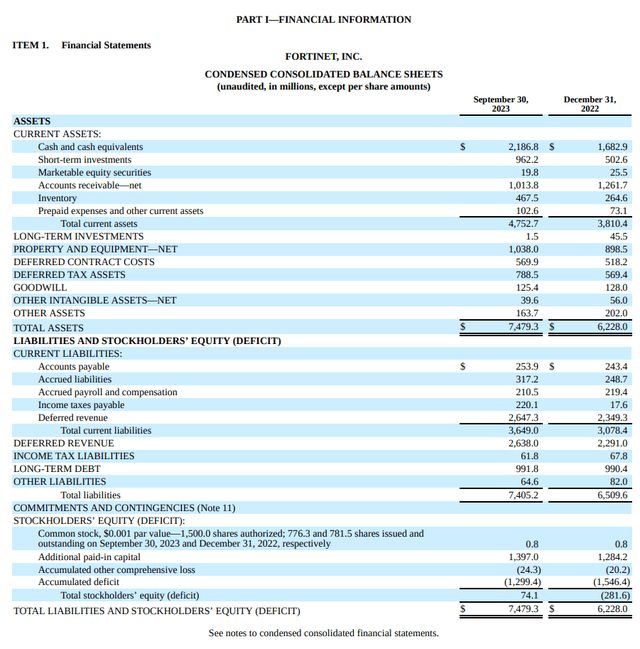

While the income and cash flow statement shows sustainable growth, profitability, and strong margins, I needed to look through the balance sheet to see if there are any red flags. FTNT has a clean balance sheet, with its largest liability being deferred revenue. FTNT has $991.8 million in long-term debt on the books with $3.17 billion in cash and short-term investments on hand. FTNT is also buying back shares, and since the close of 2019, they have repurchased 94.7 million shares or 10.98% of their outstanding shares. This company is unlevered as their liquidity exceeds their total debt by $2.1 billion and is buying back shares. This is the type of balance sheet I love to see from a company that is still in growth mode.

Fortinet

CSCO agreed to acquire SPLK for $157 per share or $28 billion. SPLK is one of FTNT’s peers, and it is currently trading at just under the acquisition price that CSCO agreed to. When I look at SPLK at its current valuation and the valuation CSCO is paying, FTNT looks grossly undervalued. It doesn’t matter what I think is the correct number, and something is only worth what someone is willing to pay for it. This is why I am looking at what CSCO is willing to pay for SPLK compared to where FTNT is trading. SPLK is trading at 30.22x its TTM FCF, and based on the $28 billion price CSCO agreed to, they are paying 32.96x for SPLK’s FCF. FTNT generated an additional $1.21 billion in FCF compared to SPLK in the TTM and is trading at 21.78x its FCF. This looks extremely cheap as CSCO was willing to pay more than 30x for one of its peers. When I looked at their forward earnings estimates, FTNT and SPLK trade at similar forward P/E levels, and both are expected to grow their EPS between 25-30% over the next 2 years. SPLK looks a bit cheaper on an EPS level, but as FTNT buys back shares, this metric can certainly change.

Steven Fiorillo, Seeking Alpha Steven Fiorillo, Seeking Alpha

FTNT’s peers which have a larger market cap, are CrowdStrike (CRWD) and Palo Alto Networks (PANW). What’s interesting is that CRWD has a market cap of $61.31 billion, yet it only generates $913.1 million in FCF, placing FCF multiple at 67.15x. PANW has the largest market cap of $92.97 billion and generates $2.92 billion in FCF, placing its multiple at 31.81x. Based on the FCF multiple that PANW and CRWD trade at and the FCF multiple that CSCO is paying for SPLK, I believe there is no reason why FTNT shouldn’t trade for at least 30x its FCF.

Steven Fiorillo, Seeking Alpha

Risks to investing in Fortinet

While FTNT looks like a promising investment, its results have varied from time to time due to macroeconomic and regional economic challenges. When recessions or other economic downturns occur, companies are less inclined to spend, and factors such as inflation and higher interest rates can deter companies from making large capital investments. We have also incurred supply chain shortages that impacted technological hardware, and with geopolitical conflicts on the rise, there is no telling what impacts global supply chains incur in the future. FTNT also faces risks of not protecting against future threats and having its reputation as a leader in the industry tarnished.

Conclusion

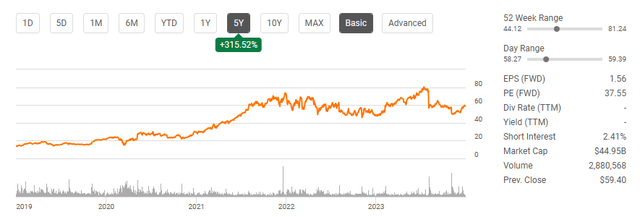

Shares of FTNT have traded sideways for the past 2 years and have just started to rebound off their 52-week lows. Shares of FTNT are still off their 52-week highs by 27.95%, and I think shares can close the gap in 2024 as this is a company that is still growing and operates in an industry with a growing TAM. FTNT is a high-margin business with a strong balance sheet and trades at a low valuation compared to its peers. I wouldn’t be surprised if further consolidation occurs and if a larger company acquires FTNT or if FTNT gets back to its all-time highs. I am not a shareholder, but I plan on starting a position as I see a lot of value in FTNT’s current valuation.

Eugen Boglaru is an AI aficionado covering the fascinating and rapidly advancing field of Artificial Intelligence. From machine learning breakthroughs to ethical considerations, Eugen provides readers with a deep dive into the world of AI, demystifying complex concepts and exploring the transformative impact of intelligent technologies.