")

JHVEPhoto

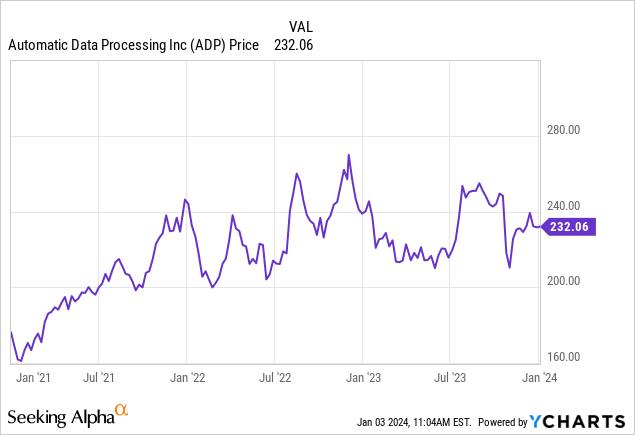

My objective with this thesis is to highlight Automatic Data Processing’s (NASDAQ:ADP) diversification strategy together with its ability to consistently hike dividends as positives for the stock going into 2024. On top, it has AI potential too, and trades at around $232 which is below its December 2022 high of $269.9 by over $36 as per the chart below. The price performance covers a three-year time horizon including 2022, when the Federal Reserve hiked interest rates at an unprecedentedly aggressive pace, with the opposite expected for this year, possibly with three cuts.

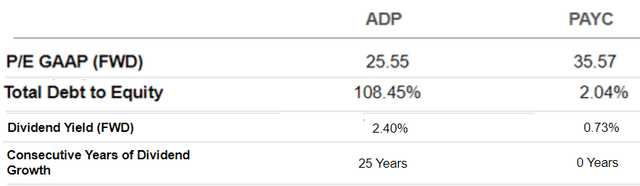

The stock remains overvalued based on metrics from the industrial sector, but, a more precise comparison of the financial performance with Paycom (PAYC), another cloud-based payroll service provider helps to show ADP’s upside potential.

I start by analyzing demand which now depends more on cyclicality, in addition to the secular trend of outsourcing versus do-it-yourself as corporations concentrate on core operations while navigating through an increasingly complex corporate world.

A Nuanced Demand Environment for HCM

First, cyclicality is related to the effects of macroeconomic changes on corporations, and currently, the talk is mostly about high-interest rates and increasing borrowing costs. This in turn makes financial conditions more difficult for companies with unhealthy balance sheets which face higher risks of becoming insolvent. In this case, according to Danyal Hussein, speaking during an investor conference on November 16, while demand is more nuanced than it was in the past several quarters, two key metrics, namely bankruptcy rates and new business formations remain healthy, auguring well for ADP.

Another moderately supporting factor is the relatively high wage inflation which reduces the recruitment appetite of ADP’s customers thereby making them more likely to rely on the outsourced payroll services. Still, ADP’s financial performance remains connected to GDP growth, and with the U.S. economy anticipated to slow down this year compared to 2023, demand is expected to trend softer and is also conditional to a soft landing which is an economic scenario where a recession is avoided.

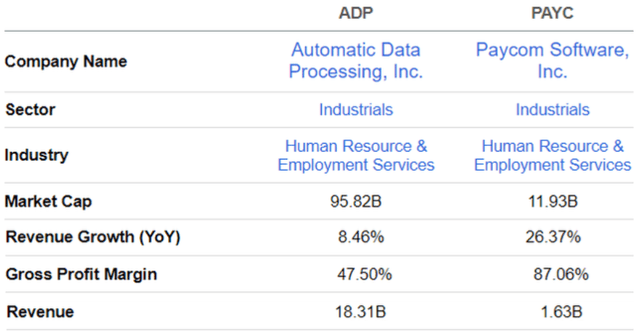

Focusing on the HCM (Human Capital Market), it can be envisioned as consisting of three tiers, the high, mid, and low end where there is competition both from private providers and publicly listed ones like Paycom. Here, its superior gross margins compared to ADP as shown in the table below, tend to indicate that most of its clients are relatively “larger brands”, a fact confirmed by a USA Today report. These tend to generate more profits for Paycom thanks to more cross-selling opportunities within the same customer base. Also, its higher revenue growth indicates that it has leveraged on more commoditized products, such as the “Beti do-it-yourself payroll” for clients whose own employees perform payroll.

www.seekingalpha.com

On the other hand, ADP’s lower margins tend to show that it has “broadened its exposure” over the years to include more small to midsize companies. Thus, its marketing team has to work harder to drive sales from a relatively larger number of firms, resulting in lower sales per customer and profitability, but this is changing as I further elaborate upon later. As for ADP’s lower growth, this is mostly explained by its incumbent position and a revenue level that is already over ten times its peer as shown above.

ADP Offers A More Diversified Approach and Dividend Growth

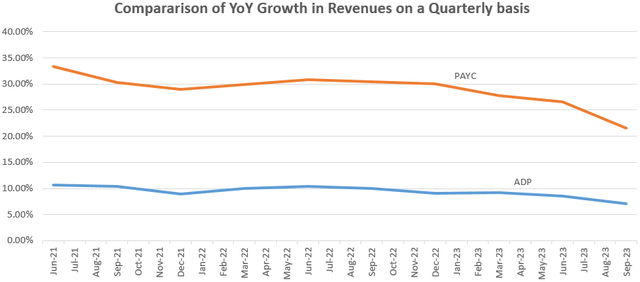

Now, it is precisely this broader exposure or more diversified approach that has helped it to mitigate the effects of uncertainty as seen by its relatively flatter YoY revenue decline from June 2021 to September 2023 as pictured in the blue chart below. In contrast, Paycom has suffered from a steep decline in YoY quarterly revenue growth as shown in orange.

Charts Built using data from (seekingalpha.com)

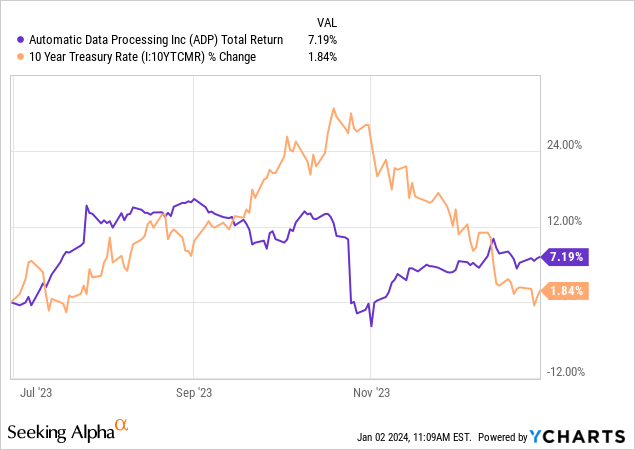

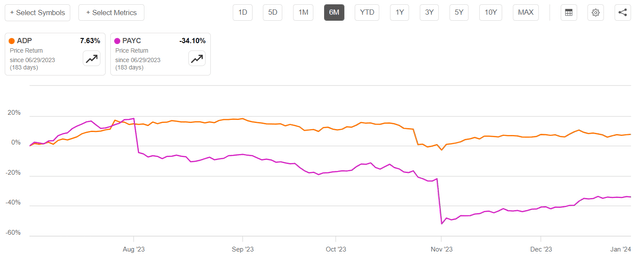

Looking further, in addition to purely financial metrics like revenue or profitability investors tend to value a stock like ADP also because of its dividends. In this respect, its forward yield of 2.4% is well below the risk-free yield of the U.S. 10-year treasury bond yield which pays above 3.75%. However, the distributions shareholders receive have consistently increased over the last consecutive 25 years which qualifies it as a dividend aristocrat. In contrast, for the 10-year, yields have been on a downtrend since the end of October as shown in the orange chart below due to the Federal Reserve switching to “pause mode” after aggressively hiking rates since March 2022.

Conversely, the Fed’s pause has benefited ADP’s stock as per the blue chart above, and, this after the stock suffered from volatility after missing topline expectations on October 25. As for Paycom, since it pays yields of only 0.73%, the downside suffered by its stock after posting mixed third-quarter results on October 31 has not been attenuated as for ADP as it does not present any rate sensitivity characteristic. Thus, Paycom’s stock which tumbled by more than 25% following results still bears the marks of acute volatility as illustrated in the purple chart below.

seekingalpha.com

Valuing ADP Considering Opportunities and Risks

Therefore, with the company’s broader exposure making it relatively more resistant to the effects of cyclicality, and the Federal Reserve widely expected to cut rates in 2024, the stock should trend higher. For this purpose, according to the US Bureau of Labor Statistics, the number of job openings on the last business day of November stood at 8.8 million, which is less than the 8.85 million openings in the previous month. This implies that the economy is slowing and reduces the probability of a rate hike.

To provide an estimate of a potential upside as to ADP’s stock, I consider that its forward GAAP price to earnings of 25.55x is trading at a discount of 28% ((25.55-35.57)/35.57)) relative to Paycom. Assuming an upside of just 10% or a P/E of 28.1x (25.55 x 1.1), which is still below the five-year average of 29.1x, I obtained a target of $255 (232 x 1.1).

seekingalpha.com

This is a conservative figure given that we are not yet out of the woods concerning inflation which is currently at slightly above 3% and remains well above the Fed’s target of 2%. Thus, the U.S. Central Bank may have to keep monetary policy tighter for longer which would partially offset the ADP rate sensitivity advantage. In such a scenario, a debt-to-equity ratio of above 100% as tabled above may deter risk-averse investors looking for a rock-solid balance sheet.

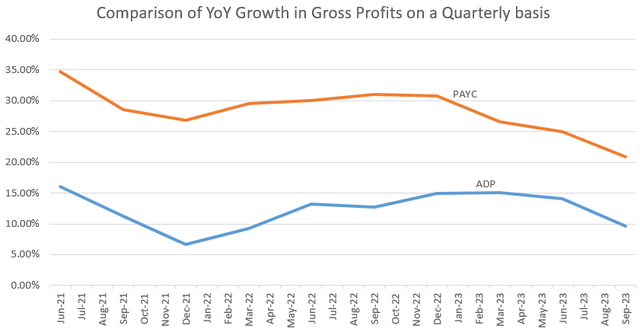

Still, for others focusing on its A+ profitability grade, a comparison of the YoY growth in gross profits in the chart below shows that, while Paycom has seen a profitability decline by nearly 15% from June 2021 to September 2023, things have been more nuanced for ADP which has seen its figures decrease by only about 5%. This may be due to its broader market presence decreasing the likelihood of facing a copycat competitor potentially eating into its market share and having to provide discounts to maintain sales targets.

Charts Built using data from (seekingalpha.com)

Therefore, for ADP, it is about being appropriately positioned to mitigate the effects of cyclicality on the one hand while continuing to benefit from the secular digital transformation on the other. This increases the likelihood of the company achieving topline growth expectations of 6.26% for FY-2024 which ends in June.

This digitalization trend which was accelerated by the pandemic, could this time receive an impetus by the drive to automate business operations using artificial intelligence after the rapid popularization of ChatGPT with its user-friendly Chatbot.

Concluding with the AI Narrative

Thus, according to a study by McKinsey on Generative AI, billions of dollars of productivity gains are possible in areas ranging from sales and marketing to customer operations, without forgetting software development. Now to translate this opportunity to reality, companies have been investing either to build their infrastructure or lease them for public cloud providers in the form of AI-as-a-Service.

In this respect, one of the advantages for smaller businesses to stick with ADP is that they do not need to invest in costly intelligent innovation but can instead benefit from Generative AI being directly embedded into product offerings as of the first quarter of 2023 which lasted from June to September 2023. In consequence, since the product is not monetized separately, existing users just need to log in to the payroll service provider’s platform.

Therefore, more than before, instead of trying to manage HR on their own, both due to compliance requirements with local and federal regulations, and from a technological complexity perspective, it makes more sense for companies to use ADP’s platform. As a result, they can free themselves focus on their core business, and get more productive. In this respect, as per Gartner, global spending on software and IT services should total $2.6 trillion in 2024 compared to last year and should be led partly by the need for more efficiency and automation. Consequently, there are additional sales opportunities for ADP as it leverages Gen AI to sign additional subscription plans or retain customers with its ability to offer AI-embedded products across the entire client life cycle.

Finally, depending on the execution of Gen AI which I have not factored in the valuations, the stock has room for further upside than the $255 target I provided. As such, given its rate sensitivity, it could again rise to the $269-$270 level following a rate cut.

Eugen Boglaru is an AI aficionado covering the fascinating and rapidly advancing field of Artificial Intelligence. From machine learning breakthroughs to ethical considerations, Eugen provides readers with a deep dive into the world of AI, demystifying complex concepts and exploring the transformative impact of intelligent technologies.