")

JHVEPhoto

A lot of stocks in the chip sector faced a brutal 2023 before a strong year-end rally. Qualcomm (NASDAQ:QCOM) was a prime example of the weakness with the wireless chip stock hit with a dip below $100 after peaking above $180 the year prior. My investment thesis remains ultra Bullish on the chip company due to the shift away from handsets and the ongoing reliance by Apple (AAPL) for modem chips.

Source: Finviz

Powering The Future

Qualcomm just launched new mixed reality chips with prime customers from Samsung (OTCPK:SSNLF) to Google (GOOG). The Snapdragon XR2+ Gen 2 chip supports 4.3K per eye resolution and 12 or more concurrent cameras to deliver crisp, immersive MR/VR experiences.

Qualcomm vice president and general manager Hugo Swart said the following about the chip:

Snapdragon XR2+ Gen 2 unlocks 4.3K resolution which will take XR productivity and entertainment to the next level by bringing spectacularly clear visuals to use cases such as room-scale screens, life-size overlays and virtual desktops. We are advancing our commitment to power the best XR devices and experiences that will supercharge our immersive future.

The company has long been working the Meta Platforms (META) on Quest AR/VR devices providing Qualcomm with a leadership position in the AR/VR chip segment. The big question is whether the Vision Pro device from Apple is able to scale to any meaningful volumes to compete with the products from Qualcomm customers.

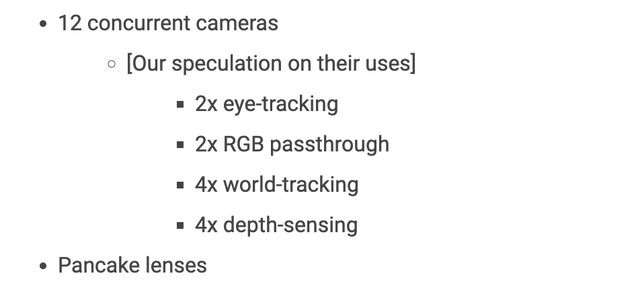

Road to VR speculates on the cameras and lenses for the reference headset released by Qualcomm as follows:

Source: Road to VR

The speculation here is that Samsung and Google in partnership are about to release an MR headset targeting the Vision Pro market. Either way, Qualcomm remains positioned to thrive when the AR/VR device market eventually takes off.

The current speculation is that Apple will release the Vision Pro in the next month or so, but the constant delays of the tech giant have opened the door for other technology companies to catch up. In an odd move, Apple actually announced the device at the Worldwide Developers Conference back in June providing competitors plenty of time to catch up with Samsung/Google able to gauge the features from the Vision Pro most desired by consumers.

Trending Higher

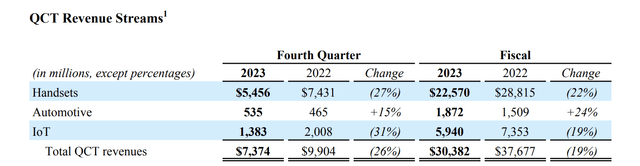

Qualcomm is busy trying to power both AI devices and AR/VR devices with modern chips along with feeding off the surging demand for tech content in vehicles. The chip company already had a promising IoT business with $7.4 billion in FY22 revenues until Covid pull forwards led to a collapse in demand last year with sales slipping to $6.0 billion.

Source: Qualcomm FQ4’23 earnings release

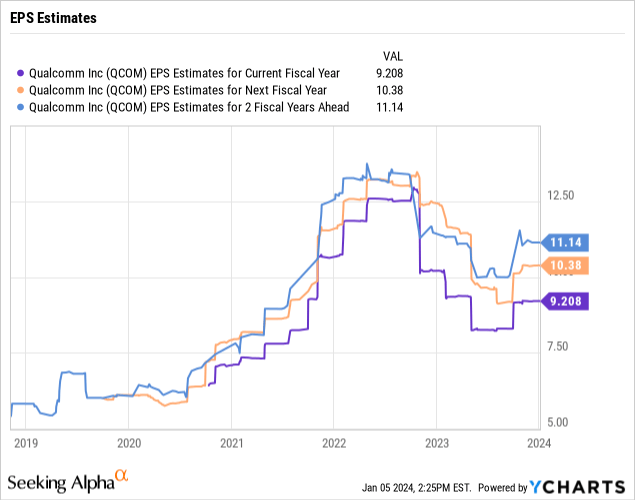

The consensus analyst estimates have started trending higher again with smartphone demand picking up and Apple remaining a modem customer though FY26. The FY25 EPS targets are now back above $10 while the stock trades below $140.

Our view is that Qualcomm has the potential to substantially boost the EPS targets with the limited growth forecasts easily exceeded. Remember, the chip company has already outlined orders in the automotive segment leading to sales growing from under $2 billion reported in FY23 surging to $4 billion in FY26 based on a total contract book topping $30 billion.

Qualcomm produced $35.8 billion in revenues during the just ended FY23, yet the consensus estimates for FY26 are just $43.5 billion for total growth of a meager $7.7 billion during the 3-year period. Heck, the wireless chip giant did $44.2 billion in sales in FY22 in a sign of the conservative view on current targets for FY26 revenue to still trail the peak numbers.

As highlighted in the prior research, Qualcomm is working on AI-chips for devices from laptops to smartphones and IoT devices. The chip company will boost revenues via these device-level AI chips plus AR/VR devices on top of the already outlined $2+ billion revenue gains from the automotive segment. An eventual rebound in smartphone sales is another path to sales growth.

Takeaway

The key investor takeaway is that Qualcomm has multiple paths to generate substantial revenue growth over the next few years. The consensus estimates appear to under estimate the growth opportunity as the wireless chip giant should sail past the FY22 numbers in the next few years.

The stock is cheap at below 13x FY25 EPS targets while the numbers appear very conservative.

Eugen Boglaru is an AI aficionado covering the fascinating and rapidly advancing field of Artificial Intelligence. From machine learning breakthroughs to ethical considerations, Eugen provides readers with a deep dive into the world of AI, demystifying complex concepts and exploring the transformative impact of intelligent technologies.